As Credit score Counsellors, we’re usually requested, are you able to consolidate debt right into a mortgage? The thought is that in doing so, you’ll scale back the general curiosity it’s important to pay in your particular person money owed (as a result of the mortgage price ought to be decrease) and unencumber doubtlessly a whole lot of {dollars} each month.

It’s a win-win, proper? Not so quick.

Generally, consolidating debt right into a mortgage can value you. However first, let’s check out simply the way it works.

Understanding Debt Consolidation Mortgages & The way it Works

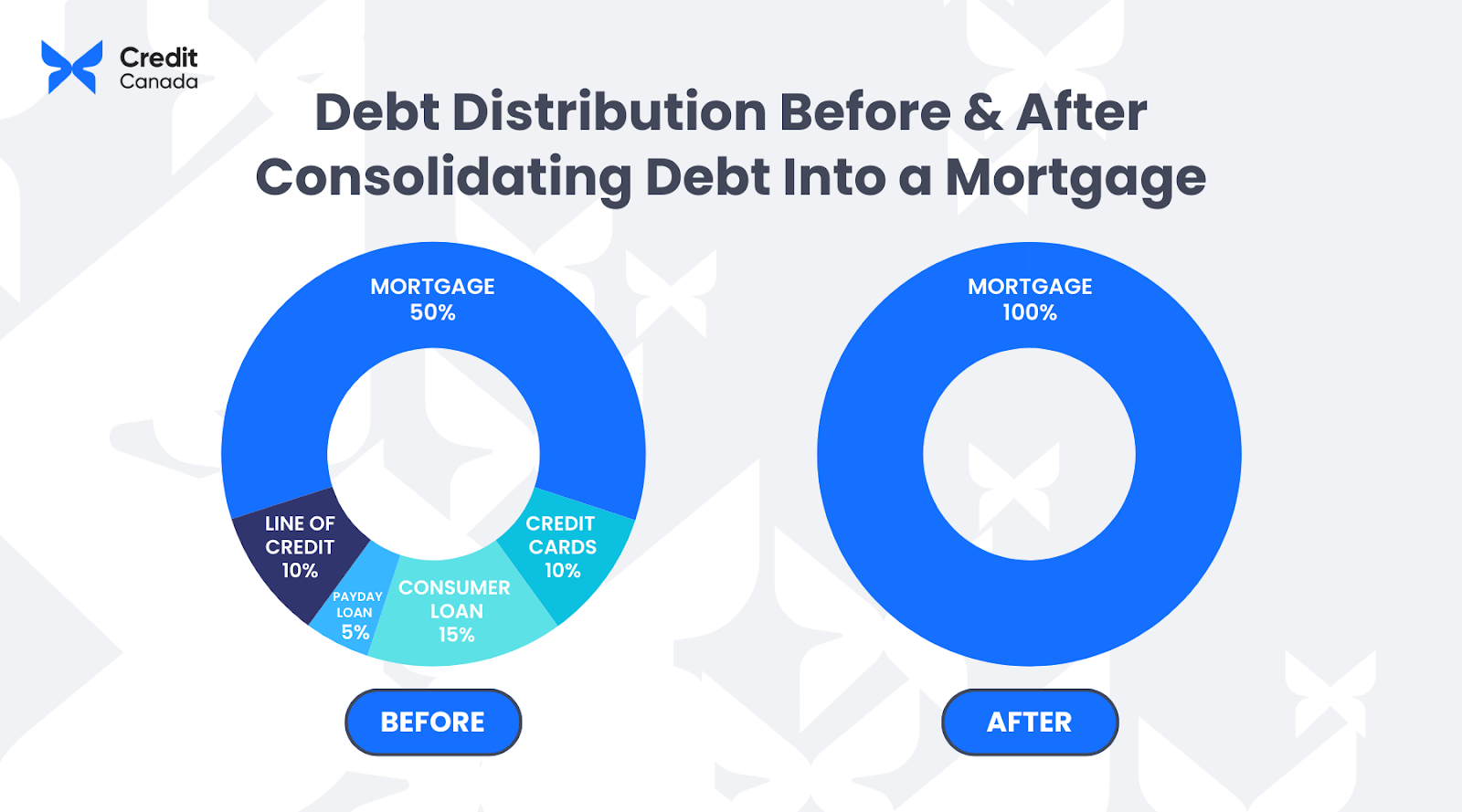

Debt consolidation is the apply of taking a number of sources of debt and mixing them right into a single account. On the subject of consolidating debt right into a mortgage, this usually means rolling your present mortgage settlement and your high-interest money owed (reminiscent of bank card debt, payday loans, and different non-mortgage balances) into a brand new mortgage set at a brand new (hopefully decrease) rate of interest. That is doable as a result of most houses have fairness in them. Fairness is the distinction between the worth of the house and what’s owed on the mortgage.

For instance, say your house is value $700K and also you solely owe $500K on the mortgage. Which means you may have $200K value of fairness. Even higher, as you proceed to pay down your mortgage, fairness continues to go up (a spike in property worth additionally will increase it, whereas a drop in property worth, after all, decreases it). That $200K is a pleasant chunk of change, proper? So on this case, you would possibly think about using it to pay down a few of your high-interest balances by selecting to consolidate your debt right into a mortgage that you just refinanced.

When you’ve achieved this, your mortgage debt will enhance by the quantity of non-mortgage debt you rolled into it, plus the price of breaking the outdated mortgage (if relevant). The upside is that, in idea, the curiosity you pay in your non-mortgage debt will lower.

Is it a Good Concept to Consolidate Debt right into a Mortgage?

Determining whether or not a debt consolidation mortgage will profit you in the long term is dependent upon many elements. Each mortgage is exclusive, and there are simply too many variables to supply a black-and-white reply—it is all gray!

For instance, some folks must take into account whether or not they may even qualify for a brand new mortgage for consolidating debt relying on the newest guidelines round mortgages right now. You even have to contemplate the brand new mortgage price you may get on the renewal. Will it’s roughly than your present price? If it is extra, does the lower in curiosity that you will pay in your non-mortgage money owed outweigh the rise within the mortgage curiosity you will find yourself paying? Earlier than you consolidate your debt right into a mortgage, these are all questions you actually need to contemplate!

There’s additionally the price of the penalty for breaking your present mortgage, in addition to any authorized charges concerned. In some instances, your property would possibly must be assessed, and that may value you some cash too.

These are all belongings you’ll want to consider to essentially know if consolidating debt into your mortgage is your best option for you. If you wish to know what the affect of selecting to consolidate debt into mortgage funds will appear to be for you particularly, you would possibly need to take into account talking together with your financial institution or credit score union, in addition to a mortgage dealer who will present an total image of accessible choices primarily based in your monetary state of affairs.

Can You Consolidate Debt right into a First-Time Mortgage?

What in the event you’re not a present home-owner, however are enthusiastic about shopping for a house? You could possibly consolidate your debt right into a mortgage when buying a brand new residence. To be eligible, lenders will take a look at your loan-to-value (LTV) ratio to find out the chance you pose as a borrower. LTV is the dimensions of your mortgage in comparison with the worth of the house you propose to purchase.

So, in case your LTV is underneath a certain quantity (sometimes 80% or much less) your lender might help you roll high-interest balances into your lower-interest residence mortgage. This may be an effective way to get out from underneath high-interest-rate loans or bank cards.

Execs and Cons of Consolidating Debt into Mortgage

There may be many advantages to utilizing mortgage consolidation and refinancing to maneuver your unsecured, high-interest money owed into your mortgage — in some instances, you could possibly save a few hundred {dollars} a month over the lifetime of your mortgage! Nevertheless it additionally has its downsides.

Advantages of Consolidating Debt right into a Mortgage

1. Diminished Curiosity Charges

Consolidating debt into your mortgage is usually a sensible transfer as a result of it usually means decrease rates of interest. This may prevent cash in the long term by lowering the quantity you pay in curiosity every month.

2. Simplified Funds

One other advantage of rolling your debt into your mortgage is simplified funds. As a substitute of juggling a number of payments with totally different due dates and rates of interest, you will have only one easy-to-manage fee every month.

3. Improved Money Movement

Consolidating your debt into your mortgage can increase your money circulation by lowering your month-to-month funds. With decrease rates of interest and doubtlessly longer reimbursement phrases, you will have extra earnings every month to cowl important bills or save for the longer term.

Downsides of Consolidating Debt right into a Mortgage

1. You may be in debt longer

By rolling different money owed into your mortgage, you’ll be paying them off over an extended time period, so you will not be debt-free any sooner.

2. You might run out of fairness

Some folks start seeing their residence as a useful resource they’ll faucet into each time they want it. In some instances, they’ll even begin treating their residence prefer it’s an ATM. However fairness will not be an infinite useful resource. If you happen to deplete your house fairness, you could not have any left when you actually need it, reminiscent of throughout a job loss or medical emergency.

3. You might rack up extra debt

In accordance with Equifax Canada’s client credit score tendencies and insights report, Canadian client debt rose to $2.4 trillion in 2023. With a mean debt load of roughly $21,131 (excluding mortgages), the info revealed Canadians are utilizing bank cards extra–and consolidating debt with a mortgage does not at all times assist curb spending.

Many individuals proceed to make use of their bank cards after consolidating their balances into their mortgage. So now, not solely are they paying extra on their mortgage, however they’ll even be again within the gap with bank card corporations.

When Can You Consolidate Debt right into a Mortgage?

In fact, there’s additionally no assure you will qualify to consolidate non-mortgage debt into your mortgage. If you happen to’re questioning, “How a lot can I borrow towards my residence,” each lender is totally different and each borrower is totally different. Deciding when it is sensible to consolidate debt into your mortgage sometimes is dependent upon the worth of the house, how a lot debt you are trying to consolidate into your mortgage, and the way a lot fairness you may have within the residence. Even when your credit score rating will not be the most effective, do not let this maintain you again from exploring this feature.

So, earlier than you comply with any adverts that pop up after typing in one thing like “mortgage consolidation” or “consolidating debt right into a mortgage in Canada,” it’s vital to perform a little research and even converse with a monetary advisor or debt administration counsellor. Mortgage brokers can assist in lots of conditions the place you assume there isn’t a hope.

Steps to Consolidate Debt right into a Mortgage

If you happen to’re contemplating rolling your debt into your mortgage however aren’t positive the place to start out, here is how you can navigate the method:

Consider Your Monetary Scenario

First, it’s vital to take a tough look within the mirror and assess your present monetary state of affairs. Take inventory of your money owed (together with their quantities and rates of interest), test your credit score rating, and consider your house fairness. This gives you a greater understanding of whether or not consolidation is an choice.

Analysis Mortgage Merchandise

Subsequent, remember to analysis what mortgage choices can be found to you so you will discover the most effective match. Contemplate elements reminiscent of rates of interest, reimbursement phrases, and any related charges. It’s vital to take time to check merchandise from totally different lenders to make sure you make an knowledgeable resolution that aligns together with your monetary targets.

Seek the advice of a Mortgage Advisor

Earlier than signing a brand new consolidation mortgage or refinancing an current mortgage, seek the advice of with a monetary skilled. At Credit score Canada, our Credit score Counsellors can present customized, knowledgeable recommendation tailor-made to your state of affairs and can assist you navigate the complexities of debt consolidation. A mortgage advisor may help in deciding on essentially the most appropriate mortgage product and information you thru the appliance course of.

Apply for a New Mortgage or Refinance

As soon as you have chosen the precise mortgage product for you, fastidiously comply with the lender’s directions for the appliance course of and supply all mandatory documentation. Be ready for an intensive evaluation of your monetary historical past and property by the lender.

Use the New Funds Properly

Lastly, upon consolidating your money owed, use the newly accessible funds properly to maximise their affect. Contemplate specializing in constructing an emergency fund, investing in retirement financial savings, or tackling any remaining money owed not included within the consolidation.

{kind=link}

Different Debt Consolidation & Debt Assist Choices

If you happen to’re hesitant to make use of up a few of your house fairness to repay your money owed, that’s comprehensible. Thankfully, there are a selection of alternate options to getting a debt consolidation mortgage you could need to take into account. Our debt consolidation calculator can provide you a tough thought of how lengthy it should take you to repay your unsecured money owed at their present rates of interest utilizing totally different reimbursement methods. The calculator additionally supplies totally different debt reduction choices which may be accessible to you reasonably than consolidating your debt into your mortgage.

Residence Fairness Line of Credit score (HELOC)

Just like a house fairness mortgage, however as an alternative of getting a lump sum a HELOC is a revolving line of credit score (just like a bank card). Which means you may have entry to a sure sum of money that you should utilize as wanted, solely paying curiosity on what you borrow.

The draw back is that HELOC rates of interest are variable, that means they may go up and, as with a house fairness mortgage, undisciplined spenders might faucet out their residence fairness.

Debt Consolidation Mortgage

If you happen to’re not eager on borrowing towards your house, you could possibly get a debt consolidation mortgage by way of a financial institution, credit score union, or finance firm. A debt consolidation mortgage can be utilized to repay unsecured money owed, leaving you with just one month-to-month fee to a single lender, hopefully at a decrease rate of interest.

Nonetheless, to acquire a debt consolidation mortgage you will need to have good credit score, collateral, or a co-signer with good credit score. In some instances, a secure supply of earnings can also be wanted.

As with residence fairness loans and HELOCs, some folks can run into hassle in the event that they proceed to make use of their bank cards, whereas additionally owing to the debt consolidation mortgage lender. Nonetheless, this can be preferable to signing a brand new consolidation mortgage or refinancing an current mortgage to cowl high-interest balances for some.

Price range Planning

Okay, this isn’t a debt consolidation choice, however we’d be remiss to not embody it! Usually, reasonably than persevering with to borrow, folks can get a deal with on their debt by training higher cash administration expertise. This consists of budgeting and watching the way you spend your cash. You are able to do this on-line with our free, downloadable Price range Planner – it’s straightforward to make use of and the directions are included within the spreadsheet.

Get Debt Reduction At present

If a debt consolidation mortgage and the opposite choices talked about above don’t curiosity you, otherwise you assume poor credit score will maintain you again, a Debt Consolidation Program is one other nice debt reduction choice.

A Debt Consolidation Program includes rolling your whole unsecured debt into one month-to-month fee by way of a non-profit credit score counselling company like Credit score Canada. An authorized Credit score Counsellor will then contact your collectors, in your behalf, to decrease your month-to-month fee and scale back or cease the curiosity in your debt.

The most effective half is that you do not want good credit score to qualify for a Debt Consolidation Program. All it’s essential give attention to is making your new, decrease month-to-month fee each month on time and in full. Our workforce may give you steerage on how you can rebuild your credit score and handle your cash. It is a win-win throughout the board and a fantastic various to consolidating debt into your mortgage. You’ll be able to hear from a few of our purchasers right here!

If you happen to’re on the lookout for some free knowledgeable recommendation on what is likely to be the most effective debt reduction choice for you given your monetary state of affairs, give us a name at 1.800.267.2272 and have a free counselling session with certainly one of our licensed Credit score Counsellors. You may get all the knowledge it’s essential make the most effective resolution for you!